Can Caribbean carriers stop losing ground?

A radical restructuring of the Caribbean market may be the only way to bring profitability and stability to the region’s carriers.

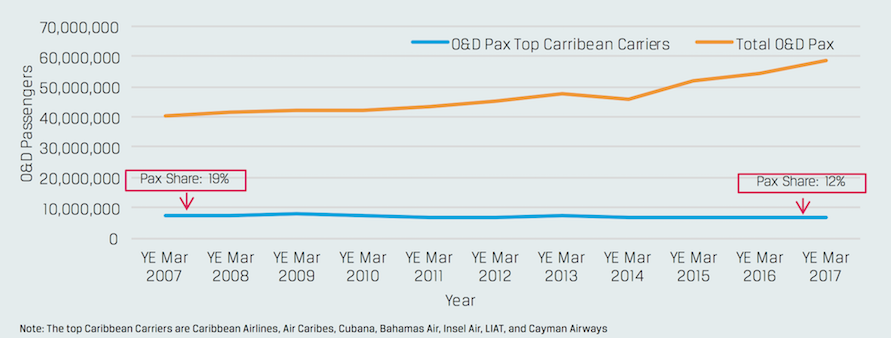

Over the last decade, the Caribbean air travel market has increased dramatically — but growth among Caribbean carriers has idled.

What accounts for the standstill? For one, the Caribbean airline industry is fragmented amongst a few local carriers which must carry passengers between many island nations dispersed over a vast region. Due to increasing foreign competition carrying inbound tourist traffic, Caribbean carriers have remained relatively niche players serving either their home customers or a limited number of intra-Caribbean passengers. Though the Caribbean air travel market has increased by approximately 50% over the last decade, Caribbean carriers’ growth has remained stagnant, and the top seven Caribbean carriers combined currently carry only 12% of total Caribbean Origin and Destination (O&D) passengers.

Caribbean O&D Passengers by Year | YE March 2007 - YE March 2017

Beyond deteriorating market share, these Caribbean carriers have largely been unprofitable. While most North American carriers have enjoyed years of strong profitability, Caribbean Airlines, the largest carrier in the region, lost an estimated $60 million in 2014. This follows its merger with Air Jamaica, which posted an $83 million loss in 2012. In 2016, Curacao’s Insel Air required a cash injection of over $16 million to stay afloat, and the struggling Bahamasair is reportedly bankrupt and requiring further government assistance.

There are a variety of factors causing the perennial struggle of Caribbean carriers:

- Foreign competition has greatly increased while the Caribbean carriers have remained stagnant. Foreign carriers, which carry a large amount of foreign- originating vacation and VFR traffic from their home countries, have been able to gain a significant amount of market share at the expense of the Caribbean carriers. This competition has also included the expansion of LCCs and ULCCs, which were almost non-existent in the region twenty years ago. Caribbean carriers with relatively high cost structures (partially due to their small size) are forced to compete in a very low pricing environment.

- U.S. consolidation has made its key players much larger, and with greater economies of scale the efficiency gap between those competitors and Caribbean carriers increases even further.

- Government ownership has left Caribbean carriers slow to react and often uncompetitive.

- Foreign carriers, including low-cost carriers (LCCs) such as JetBlue, have vastly superior onboard products, global route networks, and codeshare partnerships, which the Caribbean carriers cannot easily replicate.

- The relatively small and spread out inter-Caribbean market, combined with low overall business traffic, depresses both load-factors and yields.

- Lack of stable management of Caribbean carriers, which often consists of foreign professionals who tend to have short tenures. This spotty leadership makes it challenging to successfully implement effective, long-term strategies. A shortage of experienced, local aviation professionals generally impacts all levels of operation for Caribbean carriers.

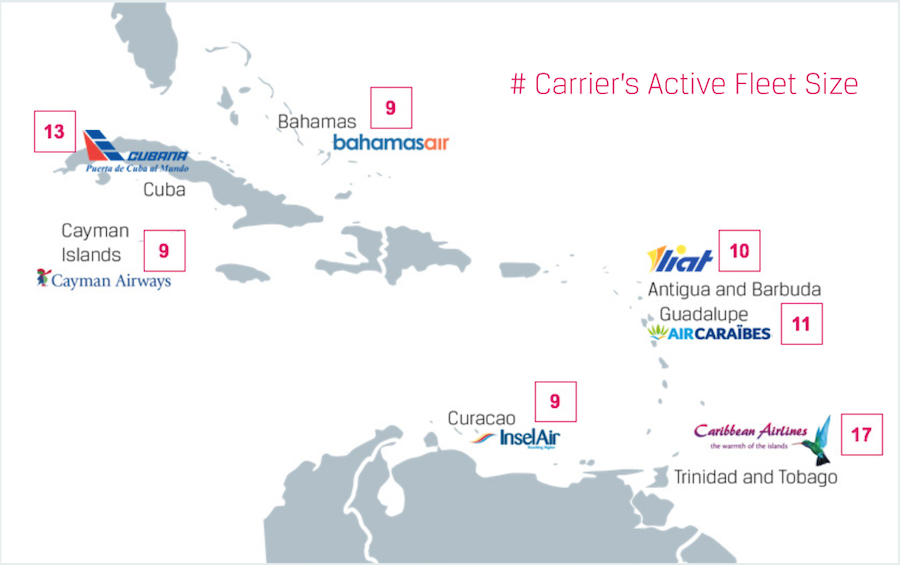

Caribbean Carriers Map and June 2017 Active Fleet Count

Fleet Count Source: CAPA Fleets

One solution to increase both scale and profitability of these Caribbean carriers would to merge many of these key players into a private pan-Caribbean airline. This integration could allow the airline to gain regional pricing power, cost efficiencies, and a significantly larger Network to seamlessly transfer passengers. Privatization would allow market forces to more efficiently allocate capacity and enable savings for taxpayers in the region. This concept has been successfully tested in South America with both LATAM and Avianca, which were able to offer much greater scale and service when combining the markets of South and Central American countries, which are more fragmented than their North American counterparts.

This solution would also need to overcome certain challenges. First, there would be major governmental rivalries and political fighting associated with the potential of certain countries losing control of air service. Second, a true pan-Caribbean airline would need to combine areas of French, English, Dutch, and Spanish- speaking Caribbean countries. These countries and travel markets often have remained culturally isolated from one other, which could be a further impediment to a unified airline. These challenges notwithstanding, a radical restructuring of the Caribbean market may be the only way to bring profitability and stability to the region’s carriers.